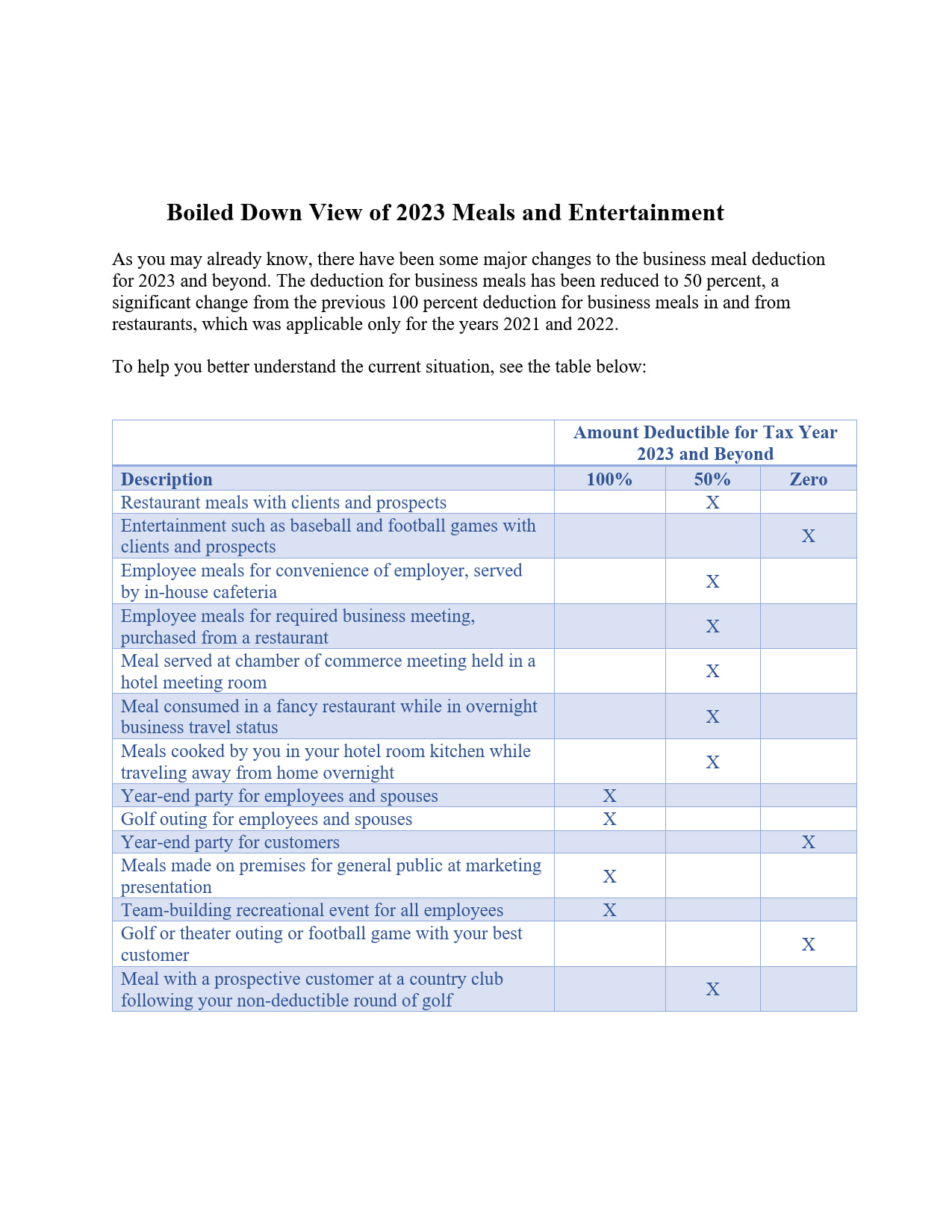

You may have heard you cannot claim a home-office deduction without business income. That’s not accurate.

Points to Consider

Action Steps

Conclusion

Your home office can provide significant tax advantages, even when your business income is low or non-existent. Make sure you position yourself to take full advantage of these benefits now and in the future.

When you own and operate a business, you must exercise vigilant oversight, including watching over your payroll taxes. Here’s an example of why.

Rodney Taylor entrusted his corporation’s accounting and bookkeeping to Robert Gard, CPA. Over several years, Mr. Gard embezzled between $1 million and $2 million, including payroll taxes.

Despite Mr. Gard’s wrongdoing, the ultimate responsibility to settle the payroll taxes with the IRS fell on Mr. Taylor as the business owner and “a responsible party” under tax law.

The Taylor case highlights a crucial lesson: while delegation of duties is a part of business, you cannot transfer your responsibility for compliance with the tax laws. Here are two proactive steps to protect your business:

By implementing these two simple measures, you significantly mitigate the risk of embezzlement and maintain compliance with tax obligations while safeguarding your financial interests and those of your company.

On January 1, 2024, the Corporate Transparency Act (CTA) was enacted. The CTA requires most smaller corporations, most limited liability companies, and other business entities to file a beneficial ownership information (BOI) report with the U.S. Department of the Treasury Financial Crimes Enforcement Network (FinCEN).

The BOI report identifies and provides contact information for the individuals who own or control the entity. FinCEN will share this information with law enforcement to combat money laundering and other illegal activities.

About 32 million existing and most new businesses are subject to this filing requirement. Since the first of the year, about 500,000 BOI reports have been filed online at the FinCEN website.

But on March 1, 2024, a federal district court (federal trial court) in Alabama ruled that the Corporate Transparency Act was unconstitutional. In National Small Business United v. Yellen, No. 5:22-cv-01448 (N.D. Ala. 2024), the court issued an injunction staying enforcement of the CTA against the two plaintiffs in the case: a single individual business owner and the National Small Business Association—a 65,000-member nonprofit organization of small business owners.

The district court ruling created some uncertainty among businesses subject to the CTA (termed “reporting companies”). Here’s what you need to know:

• If you were not a member of the National Small Business Association as of March 1, 2024, this decision has no immediate impact on you. FinCEN still expects all reporting companies to comply.

• As expected, the Justice Department, on behalf of the Department of the Treasury, filed a notice of appeal on March 11, 2024. In other words, this trial court decision is far from the final word on the CTA’s constitutionality.

• No one can predict how the courts will ultimately rule, but many legal experts believe there are substantial legal grounds to reverse the trial court’s decision.

• If your reporting company existed before 2024, you have until January 1, 2025, to comply with your BOI filing requirement. So, you can wait until late 2024 to see what happens with the pending litigation.

• If your reporting company was formed during 2024, you have only 90 days after your articles of incorporation, articles of organization, or similar documents were filed with the secretary of state to file your BOI report. You can’t afford to wait.

Meanwhile, New York adopted its own BOI reporting law that applies only to limited liability companies formed in New York or formed out-of-state that register to do business in New York. Existing LLCs must file their reports with the New York Department of State by January 1, 2025. Newly formed LLCs will file their reports when they file their articles or registrations. Other states, such as California, are considering enacting similar laws.

If you are a U.S. citizen living and working abroad, you face potential tax implications.

The United States has a taxation system that requires its citizens to report and potentially pay taxes on their worldwide income. In other words, as a U.S. citizen, you remain subject to U.S. tax obligations, even when living abroad.

Overview

As a U.S. citizen living and working in any foreign country, you can take advantage of three possible income tax breaks:

- The foreign earned income exclusion allows you to exclude up to $120,000 of your foreign income from federal income taxes.

- The housing exclusion (or deduction) allows you to exclude or deduct up to a ceiling amount of certain foreign housing costs, including rent, utilities (except telephone), and real and personal property insurance.

- The foreign tax credit allows you to reduce your taxes by the taxes you paid in the non-U.S. country where you The foreign tax credit’s purpose is to eliminate double taxation of foreign earned income. You can’t use the foreign tax credit on income you excluded using 1 and 2 above.

Foreign Earned Income Exclusion

As a U.S. citizen living and working in a foreign country, you may be eligible for the foreign earned income exclusion. This provision or deduction allows you to exclude from your U.S. taxable income a portion of the wages you earned abroad.

What Is Foreign Earned Income?

“Earned income” is money you earn for personal services performed, such as wages, salaries, or professional fees. So, “foreign earned income” is the money you earn during the period that you live abroad. To qualify for the foreign earned income exclusion, you need to have a tax home in a foreign country and to meet one of the two residency requirements discussed below.1

If you qualify, you can avoid federal income taxes on up to $120,000 of your 2023 earned income.2 Both wage and self-employment income can qualify for the “living abroad” tax breaks.

And if you’re married and both you and your spouse have income from living abroad, each of you can qualify for these tax breaks.

Tax Home in a Foreign Country

Your “tax home” (despite how it sounds) is not necessarily the physical home in which you live but is located at your regular place of business.3 For tax-free income, you want that location to be in a foreign country.

If you have no regular or principal place of business because of the nature of your work, then your “regular place of abode” (your residence) is the location of your tax home.4

During any period that your abode is in the United States, you lose your foreign-located tax home.5

The Two Residency Tests

Two primary factors determine residency overseas. One is the physical presence test, and the other is the bona fide residence test. Let’s use Germany as our example.

The physical presence test. If you have met Germany’s residency requirements, then your home is in Germany. You cannot establish residency in any other country.

To qualify for the foreign earned income exclusion, the U.S. requires that you reside in Germany for 330 days within a 12-month period.6 The 330 days do not have to be consecutive days. This affords you 35 days to vacation, live, or work as a non-resident anywhere else in the world.

If the 12-month period is from January 1 to December 31, you may take a full “exclusion” of up to $120,000 for 2023.7

If the 12-month period overlaps partially with the previous tax year, you can prorate your exclusion.8

Example. You move to Germany, and your first full day there is July 1, 2023. You meet the physical presence test for the period July 1, 2023, to June 30, 2024; therefore, the maximum exclusion you can take in 2023 is $60,000 (50 percent of $120,000).

The bona fide residence test. This test is not as desirable; you can rely on it only if you can’t meet the physical presence test. Under the bona fide residence test, you must live abroad for the entire tax year. Also, your residency must be on consecutive days. There are no days allowed for living or working in other countries.9

Please note, unlike meeting the physical presence test, meeting the bona fide residence test does not give you a prorated exclusion for your first partial year.

In order for you to pass the residency test, courts take many factors into account, including the following:10

- The taxpayer’s Is it your intention to stay in Germany where you live and work?

- Establishment of a Have you signed a lease or purchased a house in Germany?

- Location of Is your family living with you?

- Nature and duration of Do you have a contract with a German company for an extended period of time?

- Social and economic ties to the foreign country. Do you have extended family or friends in Germany?

Note: If you live abroad, you need to proactively structure your time back in the United States so that you meet the 330-day physical presence test in a calendar-year period. This ensures German residency using the safer of the two tests.

Collect the Money

Here’s a caution: to qualify for the income exclusion, you need to collect the money you earned before the end of the taxable year that follows the year in which you performed the services.11

Example. You earned the money in 2023. You need to collect the money before 2025.

NOTE: You can’t structure the pay to trigger the exclusion in the second or later year after the year you earned the money. The purpose of this rule is to limit manipulative efforts to enable the exclusion and avoid foreign taxes.

Foreign Housing Exclusion or Deduction

Want more than $120,000 of tax-free income? You can claim an additional exclusion for the cost of housing. Here’s how it works:

- Add up the expenses that qualify for the exclusion, which include rent, the fair rental value of employer-provided housing, utilities (but not telephone charges), insurance, furniture rental, repairs, and parking.12

- Take 16 percent of the $120,000 exclusion for 2023 ($19,200) and subtract it from your housing costs above.

- Claim no more than 30 percent of the $120,000 exclusion ($36,000).13

The actual computation is done daily, but what you see above gives you the basics.

Example. Say your qualified housing costs while living in Germany for the year are $60,000. Subtract $19,200 for the base housing amount, and you have $40,800. But the most you can deduct is $36,000, so your foreign housing exclusion or deduction is $36,000.

Expenses that don’t qualify for the exclusion include capital expenditures (such as the purchase of a house), mortgage interest and real estate taxes on a house you own, purchased furniture, domestic labor, television subscriptions, and deductible moving expenses.14

How Do You Take the Exclusions?

For the first taxable year for which you want to claim the foreign earned income exclusion or the foreign housing exclusion, you must elect it using IRS Form 2555; the election is valid for all subsequent years unless revoked.15

The Form 2555 election is an individual election. If spouses are claiming the exclusion for the first time on a joint return, each spouse must complete a Form 2555.

Foreign Tax Credit

Most foreign countries impose an income tax. So, you will most likely pay income taxes to the country in which you’re living and working. If you were sent to Germany, then you will pay taxes in Germany.

The United States taxes your worldwide income but allows you to minimize or even eliminate double taxation. You can do this by taking advantage of

- the foreign earned income exclusion and the housing exclusion or deduction, as discussed above or

- the foreign tax 16

As a U.S. citizen, in situations where you pay income taxes to a foreign country, often you can claim a foreign tax credit. This allows you to avoid double taxation by reducing your U.S. tax liability by the amount of foreign taxes paid on the same income.

It’s important to note that certain rules and limitations apply when claiming the foreign tax credit.

You may not claim both the foreign tax credit and the foreign earned income exclusion or the housing exclusion/deduction on the same income17. So, you must decide which of the two tax breaks gives you the better benefit.

Here is some information that will help you decide.

If you live and work abroad and you pay income taxes to a foreign country, you might end up in a better position by electing the foreign tax credit to offset your U.S. tax liability.

Also, there are several benefits to using the foreign tax credit over the foreign earned income exclusion.

Benefits of Using the Foreign Tax Credit

Here’s one advantage to using the foreign tax credit: if you can’t use the entire foreign tax credit amount in the current year due to limitations, you can carry any unused amounts back one year and, if not used, then forward for up to 10 years.18

If you elect to take the foreign earned income exclusion, you can’t get the additional child tax credit for that year.19 But if you use the foreign tax credit and you have dependent children living with you in Germany, the additional child tax credit could still be refundable assuming you do not have U.S. tax liability.20

Here’s another advantage to using the foreign tax credit: once you elect the foreign earned income exclusion, you must continue to use it unless you specifically revoke it. And once the foreign earned income exclusion is revoked, you cannot reelect it during the next five tax years unless you get consent from the IRS via a private letter ruling (generally an expensive option).21

Reporting Foreign Financial Accounts

As a U.S. citizen living in Germany, you will likely have some German bank accounts. You need to be aware of your reporting obligations regarding foreign financial accounts.

If the total combined value of all your foreign bank and financial accounts exceeds $10,000 at any time during the year, you’re required to file the Report of Foreign Bank and Financial Accounts (FBAR).22

You may also need to disclose additional information on Form 8938, Statement of Specified Foreign Financial Assets.

Tax Treaties

You’ll be interested to know that the United States has income tax treaties with many countries.23 Such treaties can impact your tax obligations. Treaties like these exist for various reasons, but mainly to prevent double taxation by promoting cooperation between countries in tax matters.

Under these treaties, you may be eligible for certain credits, deductions, exemptions, and reductions in the rate of taxes on certain items of income you receive outside the U.S.

Social Security

International agreements (known as “totalization agreements”) eliminate dual taxation on Social Security and Medicare taxes.

The United States has entered into such agreements with 25 foreign countries. Totalization agreements exempt wages from Federal Insurance Contributions Act (FICA) taxes.

This is a beneficial tax break if your earnings are subject to taxes or contributions for similar purposes under the social security system of a foreign country. A similar exemption exists if you are self-employed.

Key point. You cannot use the social security taxes paid to a foreign country as taxes paid for the foreign tax credit due to a totalization agreement, because such an agreement eliminates the double-taxation threat.

Takeaways

As a U.S. citizen, you report and potentially pay taxes on your worldwide income, regardless of where you reside. In this article you were sent to Germany and triggered the possible use of either

- the combined foreign earned income exclusion and housing exclusion/deduction, or

- the foreign tax

The foreign earned income exclusion permits you (as a U.S. citizen) to exclude up to $120,000 of your foreign earned income from federal taxes. To qualify, you need to have a tax home in Germany and meet one of two residency requirements, which involve staying in Germany for a certain duration.

The housing exclusion or deduction allows you to exclude or deduct certain foreign housing costs.

Alternatively, you can claim a foreign tax credit, which can reduce your U.S. tax liability by the amount of foreign taxes you paid to Germany. The foreign tax credit allows you to avoid double taxation. But you cannot claim, on the same income, both the foreign tax credit and the foreign earned income or housing exclusion/deduction.

The foreign tax credit has advantages over the foreign earned income exclusion because the foreign tax credit gives you —

- the ability to carry back one year (and forward for up to 10 years) unused amounts,

- eligibility for the additional child tax credit, and

- the possibility of revoking the decision (in contrast to the irrevocability of the foreign earned income exclusion).

Footnotes

- IRC Section 911(b)(1)(A).

- Rev. Proc. 2022-38; IRC Sections 911(b)(2)(D); 911(a).

- Section 1.911-2(b).

- ibid

- ibid

- Section 1.911-2(d)

- Section 1.911-3(d).

- ibid

- IRC Section 911(d)(1)(A).

- Nelson v , 30 T.C. 1151; Benfer v Commr., 45 T.C. 277 (1965); Larsen v Commr., 23 T.C. 599 (1955).

- IRC Section 911(b)(1)(B)(iv).

- Section 1.911-4(b)(1).

- IRC Section 911(c).

- Section 1.911-4(b)(2).

- Section 1.911-7(a)(1); IRS Form 2555, Foreign Earned Income (2022); Instructions for Form 2555, dated June 29, 2022.

- IRC Section 911.

- IRC Section 911(d)(6).

- IRC Section 904(c).

- IRC Section 24(d)(3).

- IRC Section 24(d).

- IRC Section 911(e)(2).

- The FBAR report is authorized by 31 S.C. Section 5314.

- IRS 901, U.S. Tax Treaties (2016), dated Oct. 12, 2016, p. 2.

Using a Vacation Home as a Rental Property and for Personal Use

When you use a home for both rental and personal use, regardless of that home’s location at the beach or in the city, you run into the tax code’s vacation home rules that make that home either a residence or a rental property.

It’s a residence when you

- rent it for more than 14 days during the year and

- use it for personal purposes for more than the greater of 14 days or 10 percent of the days that you rent the home out at fair market rates.

Example. You own a beachfront vacation condo. During the year, you rent it out for 180 days. You and members of your family stay there for 90 days. The property is vacant the rest of the year except for seven days at the beginning of winter and seven days at the beginning of summer, which you spend maintaining the property. Your condo falls into the tax code–defined personal residence because

- you rented it out for 180 days, which is more than 14 days, and

- you had 90 days of personal use, which is more than 14 days and more than 10 percent of the rental days.

Disregard the 14 days you spent maintaining the place.

The fundamental principle that applies when your vacation home is a personal residence is that expenses other than mortgage interest and property taxes allocable to the rental use cannot exceed the gross rental income from the property. In other words, rental operating expenses and depreciation cannot cause a tax loss on Schedule E of your Form 1040 for the year in question.

A Brief Overview of Non-Fungible Tokens (NFTs)

Did you buy, sell, donate, or receive an NFT during the tax year? If so, you must answer “yes” to the digital assets question on page one of the IRS Form 1040. Additionally, if you have sold an NFT, you could be liable for tax or eligible for a deductible loss.

If you are unsure what an NFT is, it stands for non-fungible token, meaning each NFT is unique. NFTs differ from Bitcoin and other forms of cryptocurrency in that they are non-interchangeable with other crypto or real currency. They are digital certificates of ownership for virtual or physical assets, such as digital art, collectibles, music, virtual real estate, etc.

In Notice 2023-27, the IRS said, for the time being, it will treat NFTs that are tax-law-defined collectibles as collectibles for tax purposes. This is important for the following reasons:

- If you sell a collectible held for more than one year, your maximum capital gains tax rate is 28 percent, whereas other assets have a maximum of 20 percent.

- If you have your individual retirement account (IRA) or stock bonus, pension, or profit-sharing plan buy a collectible, you are deemed to have taken a taxable distribution that is subject to ordinary income taxes and early withdrawal penalties.

The tax code defines a collectible as any work of art, rug or antique, metal or gem, stamp or coin, or any alcoholic beverage.

You buy and sell NFTs online. You typically buy NFTs using cryptocurrency, namely Ethereum. When you exchange Ethereum for an NFT, you recognize a capital gain or loss. Your later sales of NFTs also trigger capital gains or losses.

NFTs are considered non-capital assets in the hands of their creators, and hence, when sold, creators receive ordinary income. Donations of NFTs to charity result in a charitable deduction for the purchaser, but donations by NFT creators hold little value.

Additionally, personal gifts of NFTs to your relatives and others are not taxable events to the recipients.

If you realize a capital gain or loss from buying or selling an NFT, you report the transaction on IRS Form 8949, Sales and Other Dispositions of Capital Assets. The totals from this form transfer to your Form 1040, Schedule D.

You must track your NFT transactions to report them on your tax return correctly.

What You Need to Know About the IRS Trust Fund Recovery Penalty

If you are an employer who withholds income tax, Social Security and Medicare taxes from your employees’ paychecks, you have a legal obligation to pay those taxes to the IRS on time. These taxes are called trust fund taxes because they belong to your employees and the government. If you fail to pay these taxes, you may face a severe penalty known as the Trust Fund Recovery Penalty (TFRP), also known as the 100% penalty.

The TFRP is equal to 100% of the unpaid trust fund taxes. This means that if you owe $10,000 in trust fund taxes, you may also have to pay a $10,000 penalty on top of that. The TFRP is imposed on any person who is responsible for collecting, accounting for and paying over the trust fund taxes and who willfully fails to do so. This can include:

– An officer or an employee of a corporation

– A member or employee of a partnership

– A sole proprietor

– A corporate director or shareholder

– A member of a board of trustees of a nonprofit organization

– Another person with authority and control over funds to direct their disbursement

– A payroll service provider or a professional employer organization

To be liable for the TFRP, you must have acted willfully. This means that you knew or should have known about the unpaid taxes and either intentionally disregarded the law or were plainly indifferent to its requirements. For example, if you used the withheld funds to pay other creditors or expenses instead of paying them to the IRS, that would be considered willful.

The IRS can assess the TFRP against multiple responsible persons for the same unpaid taxes. This means that if you are one of several people who had control over your business’s finances and payroll, you may all be held jointly and severally liable for the penalty. However, this does not mean that each person must pay 100% of the penalty; rather, each person is liable for up to 100% of it until it is fully paid.

If you receive a notice from the IRS that they intend to assess the TFRP against you (Form 2751 with Letter 1153), you have 60 days (75 days if outside the U.S.) from the date of the notice to appeal it. You can request an appeal by filing Form 9423, Collection Appeal Request, with your local IRS office.

If you do not appeal or if your appeal is denied, then after 90 days (105 days if outside U.S.) from the date of the notice proposing assessment, the TFRP will be assessed against each responsible person by sending them Form

2751, Proposed Assessment of Trust Fund Recovery Penalty. Once assessed IRS may begin enforced collection actions against the responsible persons.

The best way to avoid facing this harsh penalty is by paying your trust fund taxes on time. However, if you find yourself in trouble with unpaid trust fund taxes and facing potential liability for TFRP, then contact us today. https://taxsolutionsatx.com. Ensure that your bookkeeper or accountant is paying the monthly or semiweekly employment tax deposits when they are due.

We can help negotiate with IRS on your behalf. You may not know that an issue exists until a Revenue Officer visits your business or home and demands immediate full payment. Revenue Officers, without exception, are aggressive individuals when it comes to collecting Trust Fund taxes, and by the time they leave, they will probably with a partial or full payment. By the time they leave, you will know that they are very serious about collecting those taxes, penalties and interest the fastest way available to the IRS.

If you are contacted by a Revenue Officer (‘RO’), call us immediately after the visit, or inform the RO that you would like an opportunity to speak with an Enrolled Agent, CPA or attorney before answering any questions. You have a statutory right to be represented.

Revenue Officers cannot seize assets (but may threaten to do so) unless IRS has previously issued a Final Notice of Intent to Levy and Your Right to a Hearing (usually Letter 1058 or LT11) and thirty days passed, and you did not submit an appeal within thirty days from the date on the Final Notice. You should always open certified mail from IRS. More often than not it benefits you to do so.

If you have already received a Final Notice of Intent to Levy and Your Right to a Hearing, and an RO visits, you should act immediately. ROs usually give you two weeks to prepare a collection information statement so they can determine your ability to pay. If you do not meet their deadline, your life may become quite complicated. If you own/operate a business, IRS expects your books to be up to date, and they will request bank statements ranging from three to six months possibly before they leave your office.

We usually receive 30+ calls daily, so leave a voice message if we cannot attend to your call. Please note that at this time we are only accepting cases from businesses and individuals that owe back taxes.

Juan Cortez, III, Enrolled Agent

Is Your Sideline Activity a Business or a Hobby?

Do you have a sideline activity that you think of as a business?

From this sideline activity, are you claiming tax losses on your Form 1040? Will the IRS consider your sideline a business and allow your loss deductions?

The IRS likes to claim that money-losing sideline activities are hobbies rather than businesses. The federal income tax rules for hobbies have been anti-taxpayer for years, and now an unfavorable change enacted in the Tax Cuts and Jobs Act (TCJA) made things even worse for 2018-2025.

If you have such an activity, we should have your attention.

Here’s the deal: if you can show a profit motive for your now-money-losing sideline activity, you can classify that activity as a business for tax purposes and deduct the losses.

Factors that can prove (or disprove) such intent include:

- Conducting the activity in a business-like manner by keeping good records and searching for profit-making strategies.

- Having expertise in the activity or hiring advisors who do.

- Spending enough time to justify the notion that the activity is a business and not just a hobby.

- Expectation of asset appreciation: this is why the IRS will almost never claim that owning rental real estate is a hobby, even when tax losses are incurred year after year.

- Success in other ventures, which indicates that you have business acumen.

- The history and magnitude of income and losses from the activity: occasional large profits hold more weight than more frequent small profits, and losses caused by unusual events or just plain bad luck are more justifiable than ongoing losses that only a hobbyist would be willing to accept.

- Your financial status: “rich” folks can afford to absorb ongoing losses (which may indicate a hobby), while ordinary folks are usually trying to make a buck (which indicates a business).

- Elements of personal pleasure: breeding race horses is lots more fun than draining septic tanks, so the IRS is far more likely to claim the former is a hobby if losses start showing up on your tax returns.

You have heard the horror stories about mail sent to the IRS that remains unanswered for months. The IRS has mountains of unanswered mail pieces in storage trailers, waiting for IRS employees to process them.

Because the understaffed IRS is having so much trouble processing all the documents it receives, you need to protect yourself when you send an important tax filing due by a specific deadline.

If you can file a document electronically, do so. The IRS deems such filings as filed on the date of the electronic postmark.

If you must file a physical document with the IRS, do not use regular U.S. mail, USPS Priority Mail, or USPS Express Mail.

When you mail a document with these methods, the IRS considers it filed on the postmark date, but only if the IRS receives it. What if the U.S. Postal Service does not deliver it or the IRS misplaces it? You will have no way to prove the IRS received it—and the IRS and most courts will not accept your testimony that it was timely mailed.

Don’t take this chance. Instead, file physical documents by certified or registered U.S. mail, or use an IRS-approved private delivery service (generally, two-day or better service from FedEx, UPS, or DHL Express) to meet the IRS “timely mailing” requirement. When you do this, the IRS considers the document filed on the postmark date whether or not the IRS receives it.

Make sure to keep your receipt.